In 2020, many economies around the world contracted due to the Covid-19 pandemic, and a large number of macroeconomic factors showed sharp declines. Indeed, global exports fell by about 7%, according to UN Comtrade data. Ukraine’s exports were only moderately affected, falling by 1.6%. This was a potential sign of strong inelastic demand for its goods. To put this into context, not only did it better the world average, but it also significantly outperformed Russia, whose exports fell by 21%.

Ukraine’s net trade balance also reduced in 2020, by about $6.3bn (Hrv190.41bn), as the decline in its imports outstripped that of its exports. Ukraine imported $53.7bn worth of goods and exported $49.2bn.

Although Ukraine was only the 46th-largest exporter globally in 2020, it does specialise in certain goods, and the world does have a reliance on Ukraine for these goods. The Russian invasion will at least affect Ukraine’s short to medium-term ability to export these commodities.

What goods does Ukraine export the most?

In 2020, Ukraine exported more than $9.4bn worth of cereals – about one-fifth of its total exports. It was the second-largest cereal exporter, behind the US. In fact Ukraine’s cereal exports were slightly higher than Russian cereal exports ($9.3bn). Iron and steel exports ($7.7bn) was another notable export commodity for Ukraine. However, in a global context, Ukraine is only the 37th-largest exporter.

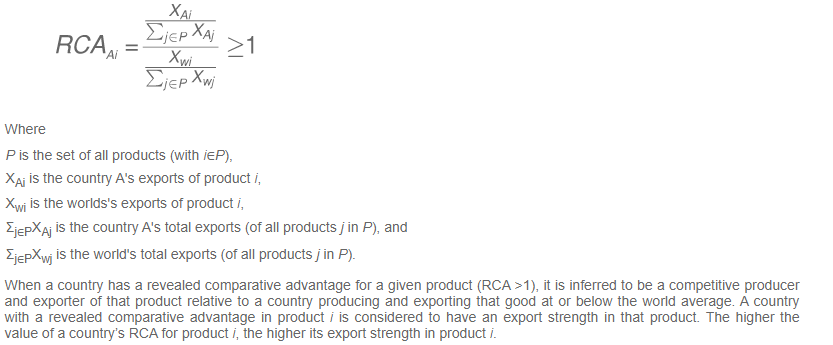

To further determine Ukraine’s commodity export prowess, we have performed a comparative advantage study to reveal the commodities in which Ukraine has export specialism. The formula for revealed comparative advantage (RCA) as per the UN Conference on Trade and Development is:

Of the 96 commodities analysed, Ukraine has a comparative advantage in 24 commodities, and it has a particular specialism in the export of cereals. The score of 27.4 indicates that Ukraine exports more than 27 times its ‘fair share’ of cereal exports.

Delving deeper within cereals, Ukraine’s cereal exports primarily involve maize, barley and wheat. The RCA scores for each of these (sub)commodities are even higher. Maize and barley score 45.9 and 41.1, respectively, while wheat and meslin scores 27.7.

In 2020, Ukraine was the:

- Fourth-largest exporter of maize globally (behind only the US, Argentina and Brazil). Ukraine exported $4.9bn worth of maize, accounting for 13% of the world’s total maize exports.

- Fourth-largest exporter of barley, accounting for 12% of total world exports, behind France, Australia and Russia. Ukraine exported larger volumes of barley compared with Australia and Russia, although its total trade value was slightly smaller.

- Fifth-largest exporter of wheat and meslin. Russia is the leading exporter of wheat and meslin, exporting an estimated $7.9bn worth in 2020. Ukraine exported $3.6bn worth.

Agriculture is important for Ukraine’s growth

Ukraine’s economy is still heavily focused on its agriculture, forestry and fishing industry. The sector has seen year-on-year growth for the past several years. Even in 2020, it grew by 9%. The industry is on track to record another strong performance in 2021. Latest figures up to the third quarter of 2021 show a 32% increase year on year compared with the first three quarters of 2020.

In 2020, agriculture, forestry and fishing was Ukraine’s third-largest sector by gross value added. Wholesale and retail trade and manufacturing were the only sectors to contribute more to the domestic economy.

Ukraine is the largest exporter globally of sunflower seeds, which it specialises in due to its favourable climate and fertile soil. In 2020, Ukraine exported $5.3bn worth. This was more than double the trade value of Russian exports ($2.5bn) – the second-largest exporter – and significantly more than other leading countries such as Turkey, the Netherlands and Hungary. Ukraine’s revealed comparative advantage score for the export of sunflower seeds was a massive 138.1.

Other key Ukrainian export commodities

When it comes to other export commodities, in 2020, Ukraine was the:

- second-largest exporter of iron or non-alloy steel (semi-finished products) ($2.7bn)

- third-largest exporter of pig iron and spiegeleisen in pigs ($922m)

- sixth-largest exporter of vegetable plaiting materials ($47m)

- ninth-largest exporter of ferro-alloys ($661m)

- ninth-largest exporter of soya-bean oil ($301m)

- thirteenth-largest exporter of rape, colza or mustard oil ($137m)

What countries will be affected if Ukraine’s exports fall?

The heat map below shows the countries to which Ukraine exports the most goods. China is Ukraine’s biggest trade partner (by exports). In 2020, Ukraine exported $7.1bn worth of goods to China, 14.5% of Ukraine’s total exports. China’s close ties to Russia perhaps outweigh any reliance it has on Ukraine. China relies on Russia for access to western European export markets and the international financial system. In terms of trade, Russian exports to China are seven times more ($49.1bn) than those of Ukraine.

Poland and Russia were Ukraine’s second and third-largest export partners, respectively, and Ukraine exported $3.3bn and $2.7bn worth of goods to these countries in 2020.

The top trade partners in 2020 for those commodities in which Ukraine had a particular export comparative advantage were:

- sunflower seeds – India ($1.4bn), China ($971m), the Netherlands ($527m)

- maize – China ($1.4bn), the Netherlands ($517m), Egypt ($508m)

- barley – China ($470m), Saudi Arabia ($118m), Libya ($70m)

- wheat – Egypt ($610m), Indonesia ($543m), Bangladesh ($295m)

- semi-finished iron or non-alloy steel – Italy ($719m), Turkey ($459m), China ($238m)

- pig iron and spiegeleisen in pigs – US ($539m), China ($201m), Turkey ($55m)

- vegetable plaiting materials – Poland ($39m), Turkey ($2m), Germany ($1m)

Which trade partners will lose out?

Ukraine is also an important country in that it imports goods from other countries. A damaged Ukraine indirectly causes damage to other economies as demand for their goods will decline. Indeed, Ukraine’s total goods imports in 2020 amounted to $53.7bn. It ranked 47th globally in terms of import trade value. Ukraine imports the most goods from China ($8.3bn worth), Germany ($5.3bn), Russia ($4.6bn), Poland ($4.1bn) and the US ($3bn).

Ukraine’s main imports include mineral fuels, nuclear reactors, vehicles, and electrical machinery and equipment. Combined, these four commodities accounted for almost half (46%) of total Ukrainian imports in 2020.

Economic powerhouses such as China and the US as well as neighbouring economies rely on Ukrainian exports:

- Mineral fuels – Russia (exports $2.4bn worth to Ukraine), Belarus ($1.6bn), US ($401m), Hungary ($395m), Lithuania ($392m).

- Nuclear reactors, boilers, machinery (and others) – China ($1.2bn), Germany ($1.1bn), Poland ($595m), Italy ($486m), Russia ($473m).

- Vehicles – US ($754m), Germany ($685m), Poland ($623m), Japan ($423m), China ($328m).

- Electrical machinery and equipment – China ($1.3bn), Hungary ($700m), Czech Republic ($543m), Germany ($418m), Poland ($410m).

Given Ukraine’s unenviable position, it is more likely to be currently demanding weaponry and aid. The above countries, among many others, will suffer if Ukraine’s fall in demand is not picked up by other countries. Some may be more impacted than others. Neighbouring countries will be the most affected as costs will likely rise, although major economies such as the US and China will likely switch to other sources.

A turbulent road ahead

Although Ukraine is a relatively small economy in terms of world trade, it is nonetheless important in several commodities. The Russian invasion will have a direct global impact on products such as sunflower seeds, maize, barley and wheat, where Ukraine has a significant comparative advantage. Ukraine is also a key player in several other commodities.

The war will heighten the already shaky economic conditions created by Covid-19. Many companies are exposed to the conflict. Supply chain problems will continue despite thoughts these would appease in 2022. Additionally, inflationary pressures will affect more countries. Furthermore, sanctions are already decimating the Russian economy, with the ruble in freefall, while companies are looking to divest. Investment conditions in eastern Europe will weaken as investors urge caution and await a peaceful outcome. Even if the invasion ends soon, for many investors political stability will significantly rise as a key site selection factor throughout central and eastern Europe.

More coverage of the Ukraine invasion from Investment Monitor: