Dynamics in the used market are set to rival the complexity of the pandemic era, according to the latest Cox Automotive’s four-year market forecast.

It predicts that a dramatic decline in new diesel cars and a reduction in petrol registrations will have a profound impact on the used market.

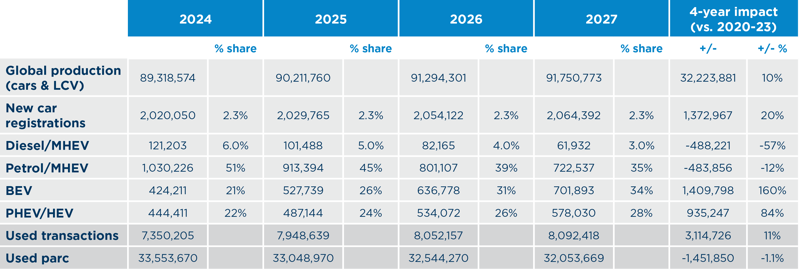

The forecast – which includes fuel-type breakdowns for the first time – indicates that in the period 2024-27, EV share of registrations will grow 160% vs 2020-23 volumes to 2.3 million units or 28% of sales.

Hybrid will represent 25% of registrations, with two million units sold. This growth comes at a significant cost for diesel and petrol derivatives.

Diesel share over the four years will shrink to just 3%, with 62,000 units registered in 2027, while petrol, with 3.5 million registrations over the four years, will fall 12% to just a 35% share by 2028.

Philip Nothard, insight director, Cox Automotive said: “The registration of the millionth EV in the UK is an important milestone in the transition to zero-emission motoring. But with two in every five new cars joining the UK car parc this year forecast to be EV or hybrid, and with that proportion destined to grow rapidly in future years, dynamics in the used market over the next four years will arguably rival the complexity and impact of those experienced during the pandemic.”

This change comes on the back of a new car market that contracted by almost a third in the four years between January 2020 and December 2023, when compared to the equivalent period 2016-19, a loss of 3.1 million cars.

The composition of the UK car parc has also changed. In 2016, EV claimed just 0.4% share and hybrid took 3%. By 2019, this had risen to 1.6% and 6%, respectively, and by the end of 2023, their share had each shot up to 17% and 20%.

The opposite can be said for petrol and diesel. In the period 2016-19, ICE cars made up 95% of new car registrations. That number fell to 71% in the period 2020-23, a loss of 4.6 million cars. The ICE decline accelerated throughout this period, dropping from an 83% market share in 2020 to 64% in 2023.

Cox Automotive forecasts a further drop of 35% between now and the end of 2027, meaning just 784,000 new ICE vehicles will hit the road in 2027 versus the 1.2 million recorded in 2023.

Diesel has experienced the most dramatic decline, from a 38% share in 2016-19, to 13% in 2020-23. By 2023, diesel vehicles – including mild-hybrid variants – represented just 8% of new registrations. Cox Automotive predicts that this share will have declined to 3% by 2028, a loss of a further 488,000 vehicles over four years, in addition to the 2.9 million lost since 2020.

At 57% in 2016- 19 vs 58% in 2020-23, petrol volumes have remained steady. Still, Cox Automotive foresees a decline over the next four-years, with its share of all registrations dropping to 51% by the end of this year and 35% by 2028. This equates to a loss of 2.3 million petrol-powered vehicles aged 0-8 years from the used market by the end of 2027.

Nothard said: “It’s almost impossible to overstate the shift in the UK car parc over the past four years and how that change will continue to accelerate. Today’s parc for cars aged 0-4 years differs significantly from 2020 and will contrast even more so in 2028.

“Manufacturers will continue to be driven by legislation rather than consumer demand and ICE will be all but gone from the UK new car market long before the 2035 deadline. For used car retailers, this means a battle for the best stock, for consumers it means diminishing choice and above-inflation price increases.”

Cox Automotive cautioned as to whether consumer demand for used EVs will reflect the pace of EV registrations in the medium term. Philip believes we will experience an increasing oversupply of EVs into the used market, at least until values become less volatile and consumer confidence grows, and price parity between EV and ICE is as likely to be driven by ICE values rising as by EV prices dropping.

Nothard added: “We must remember that in 2023, 94% of used cars sold were ICE and many consumers will likely remain loyal to this fuel type for as long as they can. The average used car buyer is often seeking to replace their existing car with something comparable that’s affordable and fits their lifestyle. They may not yet be ready to make the leap into EV for financial, infrastructure or use-case reasons.

“And while the market for used EVs will now establish itself as volumes come on stream, it faces competition from manufacturers and dealers chasing new registration volume via compelling deals and finance offers. Many potential used buyers are cautious about longer-term EV values, their comparably high outright purchase cost and the risk of technological obsolescence.

“That isn’t to say EVs don’t represent good value on the used market or will sit on forecourts unsold – in fact, there’s evidence that shows the contrary is happening. However, there is also plenty of evidence pointing to reticence on the part of private buyers while volumes in the used market are currently too small to draw meaningful conclusions.”

Nothard concluded: “This is by no means a picture of doom for the used car sector, but it would be naive to think the so-called new normal has yet been established. The overall used market is forecast to rise modestly, albeit its composition by 2028 will differ from what we’re used to today.”