With the global Light Vehicle (LV) capacity utilisation rate at a record low for this century, are we now heading for an accelerated spate of plant closures as OEMs respond by tailoring their somewhat oversized manufacturing footprints?

Certainly, when looking back at the experience of the last significant auto industry downturn, during the Financial Crisis, tumbling volumes and utilisation rates prompted an increase in plant closures as OEMs took action to cut costs and shore up losses. Indeed, in the worst affected regions – Western Europe and North America – the total number of operating LV assembly plants fell by twenty-three between 2007 and 2011, representing a 12% drop.

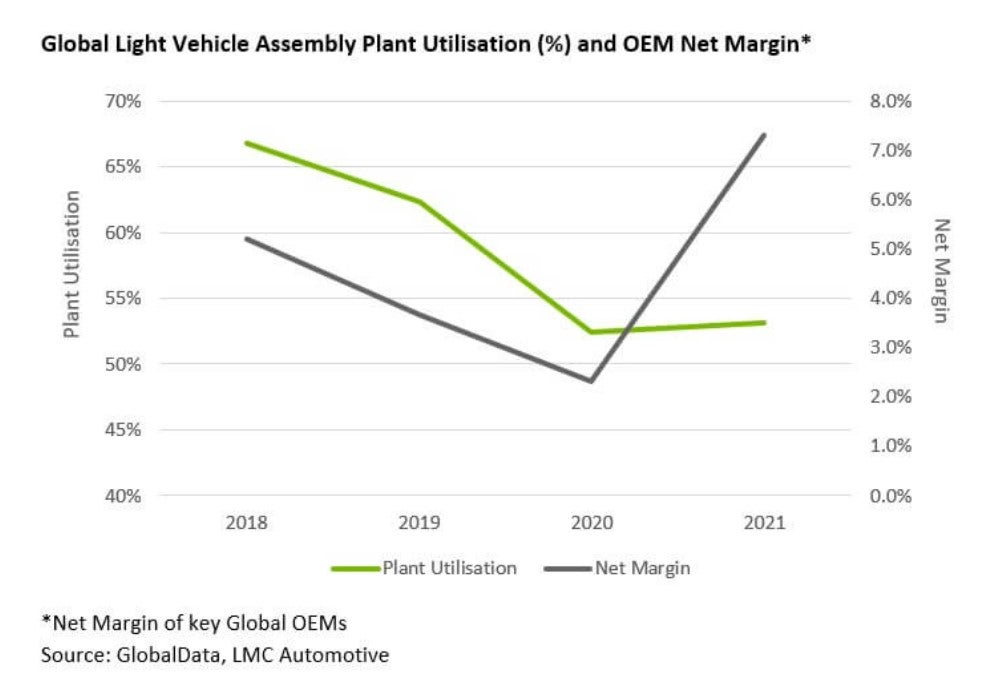

More recently, the auto industry has certainly had a tough time. COVID-19, the semiconductor crisis, and the war in Ukraine have all played their part in undermining global LV output. From its peak in 2017, global LV production slumped last year by over 20% to barely 77 mn units which has left the industry’s capacity utilisation rate languishing below 55%.

However, in contrast to the Financial Crisis, OEM margins have surged during this recent downturn as supply-side constraints have kept new vehicles scarce and transaction prices high. Flush with bumper profits, this may not be the best time politically for OEMs to implement a programme of plant closures and rationalisation. Nevertheless, with a weakening market outlook, sharply rising input costs, the challenge of transitioning from combustion to electric technologies, and a deliberate strategic shift by some brands to increasingly pursue margin over volume, OEMs may not be able to tolerate such low utilisation rates for very much longer.

Justin Cox, Global Production Director, LMC Automotive